This time is transitory

In the 2022 energy shock the 1970s burped. This time they won't.

Hello! This is the first post from Nev and Grant at Hybrid Economics.

We’ll kick off with some thoughts, drawing on a much longer piece we recently wrote for the Bain Macro Trends Group, on why the current spike in energy prices should have a very different effect on growth and inflation in Europe than the 2022 shock that accompanied Russia’s invasion of Ukraine.

Even if the rise in energy prices proves as big as in 2022, we doubt it will lead to the broad and persistent rise in inflation we saw then. Because Europe’s economies went into that shock in a very different state to today.

We’d highlight a couple of crucial differences.

First, labour markets aren’t tight.

Unemployment was at record lows going into the 2022 shock. Pandemic furlough schemes kept most workers attached to their jobs. As economies reopened, job vacancies surged. Workers briefly commanded pricing power. They demanded, and received, higher wages to compensate for higher energy costs. Those higher wages pushed up services inflation: an old-school wage-price spiral!

Today, unemployment in the UK and core Europe is significantly higher and rising. Job vacancies have slumped. Wages are slowing. Labour simply doesn’t have pricing power now to trigger a wage-price spiral.

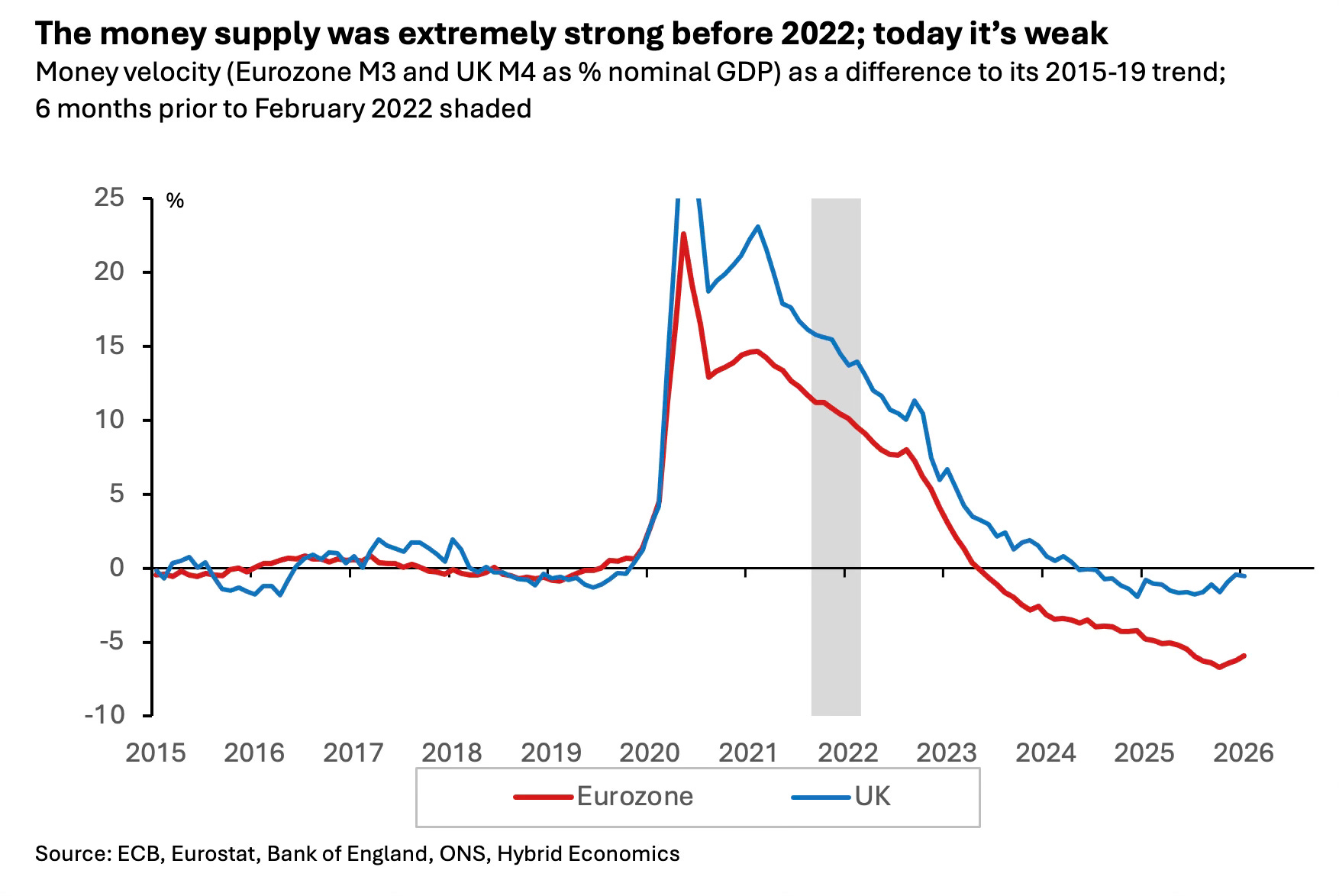

Second, there’s a lot less fuel in the system!

The money supply ballooned during the pandemic. Europe’s central banks and finance ministries conducted war finance to prevent the pandemic from triggering a catastrophic spiral of insolvency. The combination of quantitative easing, large fiscal deficits and furlough schemes transferred freshly minted central bank money to household and corporate balance sheets. Consumers and firms couldn’t spend all that cash during lockdown, leaving them with a big pile of financial dry powder as economies reopened and ultimately allowing them to absorb a large part of the shock of higher energy prices.

The chart below shows the ratio of the broad money supply to nominal GDP (or money velocity), relative to its pre-pandemic trend. The monetary, fiscal and social response to the pandemic meant the money supply was much bigger than it should have been going into the 2022 energy price shock.

That meant households and firms had excess savings they could draw down on to mitigate the hit to their living standards from higher energy prices. Consequently, too much money chased too few goods: excess money balances were spent, sustaining nominal demand and boosting inflation.

There’s no dry powder to ride out the shock today. And central banks and governments aren’t creating any. Policy rates are high (especially in the UK); the Bank of England and ECB are selling their holdings of government bonds; fiscal policy is being tightened; money supply growth is insipid.

In a way, the post-2022 inflation shock was a burp from the 1970s, with its wage-price spiral and rapid money supply growth. Inflation proved persistent because labour markets were exceptionally tight and the money supply was exceptionally strong. Strong nominal demand growth (thanks to the dry powder) and tight supply (thanks to low unemployment and jammed international supply chains) helped perpetuate the energy shock into wages, goods and services prices. Making the rise in inflation longer and stickier.

This time is different. Workers can’t command higher wages or draw on excess savings to cushion the blow of higher energy prices. That will limit the strength and persistence of inflation. But it will also mean that the hit to real spending will be greater. This is especially true if central banks, traumatised by tightening too slowly in 2022, overreact now in response to higher headline inflation.

In short: less inflation persistence; much more recession risk.

Good post and agree that the Iran war will likely prove to be more of a negative growth than persistent inflation shock to the global economy. Unfortunately he ECB and BoE don't seem to agree and are preparing the ground for rate hikes into fragile economies, especially the UK that has no growth momentum at all.