Who Governs?

The 'Bond Market' has as much wisdom and foresight as a horny teenage boy. Don't put him in charge.

Just after 8am on Friday, 8 May 2015 the Credit Suisse Fixed Income trading floor in London cheered as Ed Balls lost his seat. The Conservatives had won a surprise majority in the general election. The ‘risk’ of a Labour led-coalition was eliminated. Sterling rallied. Gilt yields fell. A bond salesman came up to me waving a Union Jack as I finished off my ‘election response’ note. It was mostly the usual sleep-deprived boilerplate, but I do remember saying that political risk had increased as there would now be a referendum on the UK’s membership of the EU. But the ‘Bond Market’ didn’t care much about that. All that mattered was that “Red Ed” wasn’t going to be PM, and their bonuses were going to be taxed less.

And here we are.

As political risks swell again, the FT has been publishing a load of articles telling us what the ‘Bond Market’ wants and thinks.

The ‘Bond Market’ likes to be taken seriously. Like it’s a proper grown up.

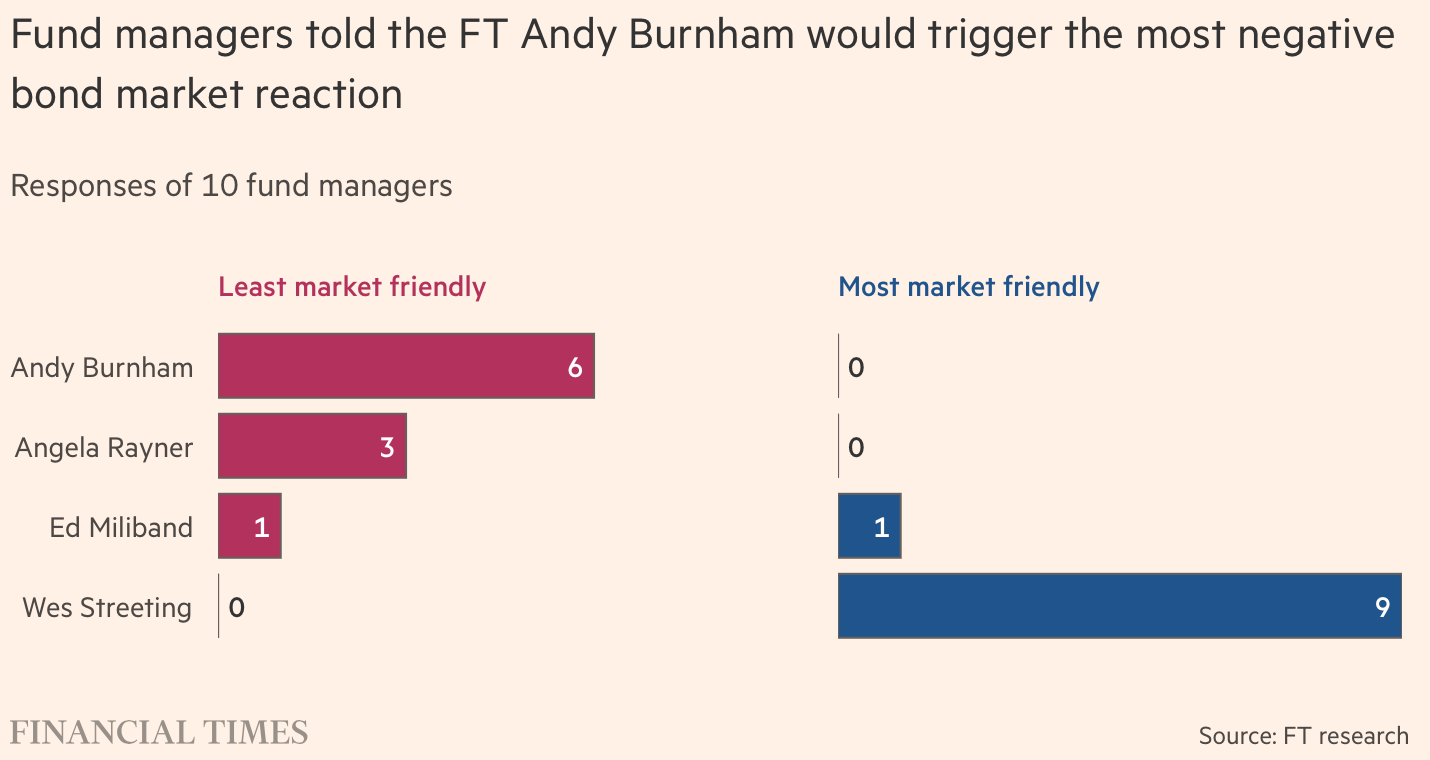

The ‘Bond Market’ LOVES Wes Streeting. But it HATES Andy Burnham. Andy once said some mean things about the ‘Bond Market’!

Pop over onto LinkedIn, and you'll see plenty of charts of the 30 year gilt yield rising to new highs, attended by breathless commentary. Now that it seems increasingly likely that Burnham will become the next PM, yields are up. You’d be forgiven for thinking the UK was a Labour Leadership Election away from financial crisis. This rather confused FT Editorial suggests that if politicians don’t do what the ‘Bond Market’ wants, then we might be.

But this is all bollocks. Everyone needs to chill out.

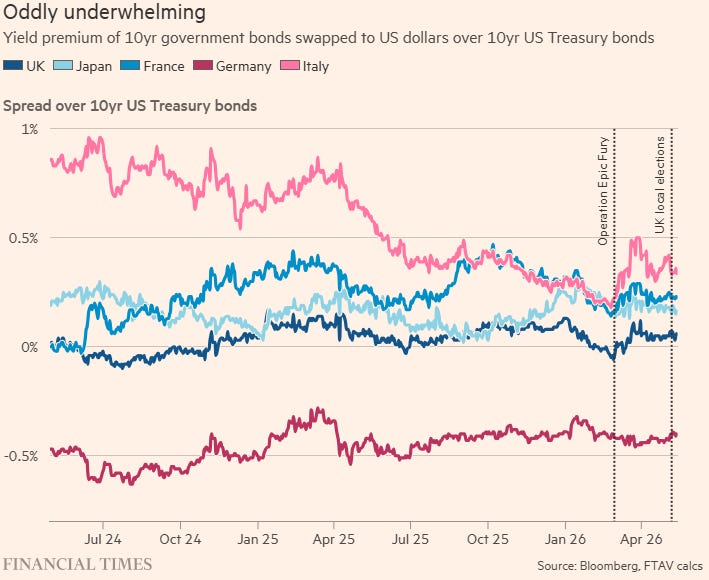

As Toby Nangle (also over at the FT) has nicely (and nerdily) pointed out there’s no evidence of a massive “plonker” premium in the Gilt market. Indeed, when Toby calculates the underlying risk premium of 10Y government bonds over that of the US (by swapping the cash flows into US dollars) it turns out that the UK has a lower risk premium than France, Japan and Italy. As he says, it’s hardly screaming plonker premium.

We’d add our own points and hobbyhorses:

First! The market for UK gilts is deep, liquid and efficient. It’s a market for financial assets, not the Fourth Horseman of the Apocalypse. Every day it balances changing supply and demand for gilts. More supply or less demand means lower prices and higher yields, and vice versa. So if the government chooses to borrow more, or the Bank of England decides to sell a truckload of gilts then the market will digest those bonds and clear at a higher yield. That’s all. It’s likely that the next PM will borrow more. All else equal, interest rates will be a bit higher than they otherwise would have been. Not ideal. But not the end of the world either.

Ah! Butwhatabout Liz Truss? Well, in the 2022 mini-budget fiscal policy was eased surprisingly aggressively when the economy was overheating, inflation was in double digits and the Bank of England was racing to hike interest rates. The gilt market didn’t anticipate such abject stupidity and had to reprice yields dramatically upwards to reflect substantially higher expectations for inflation and interest rates. The market worked. FAFO.

As we recently discussed, this time is different.

Unemployment is now rising and wage growth falling. Looser fiscal policy would nudge up interest rates. But unless the government launches a stupid massive unexpected fiscal expansion, gilt yields will be a bit, not much, higher than they otherwise would have been.

Second! That’s important because, the political economy of the UK is not good. The fiscal deficit is large. Spending cuts are politically difficult and there are existential pressures to increase spending further. But UK taxation is at its political and economic limits. The tax burden is at postwar highs. Recent tax increases have been unpopular, ineffective and impaired economic growth.

Faced with those constraints, the option to borrow more isn’t a silly one. What is the heavier burden for the UK economy. Slightly higher interest rates or another load of complex distortionary tax increases?

Third! We don’t mean to bang on about it, but… maybe the Bank of England should stop being part of the problem by continuing to sell loads of government bonds? We moaned about this in March and can’t understand why this doesn’t feature more in the debate. It’s surely not a coincidence that the UK has the highest 10Y yield and the BoE is the only G7 central bank actively selling its holdings of government bonds?

The Bank of England’s QT programme increases the supply of government bonds into the gilt market, with the inevitable consequences for yields. If the ‘Bond Market’ is worried about getting indigestion from more government borrowing, maybe it should ask why the Bank is reducing its balance sheet by £70bn of gilts a year for no good reason. This is monetary dominance over fiscal policy to the point of insanity. And it is crystallising large losses for UK taxpayers. Any competent PM or Chancellor should summon BoE Governor Bailey and tell him to stop. Or get themselves a Governor who will stop.

Fourth! If the ‘Bond Market’ thinks this lot are so bad, just wait till he meets Nigel (again). The path the UK set upon the day Ed Balls lost his seat is the main reason why the deficit is so big, taxes so high and growth so weak. What the gilt market and sterling thought were good in the short term in 2015 was utterly dreadful just over a year later. Overzealous austerity and ironclad fiscal rules have a nasty habit of delivering fiscally atrocious politics in the future.

And, just so we’re clear: outcomes that involve Nigel Farage becoming PM will be economically ruinous, just as his beloved Brexit was. Whether the “Bond Market”, many of whose participants we suspect will have taken their own personal political journey from Tory to Reform over the period since they celebrated Ed Balls’ loss in 2015, have yet to clock this is not clear.

Away from City dealing rooms, Reform’s core voter base are radicalised boomers on benefits, so there’s no chance of them cutting public spending. Political corruption and market abuse are associated with Emerging Markets, not a G7 economy. And Reform’s approach to technology - such as solar power - is luddite.

In short, much like a teenage lad, the ‘Bond Market’ massively overestimates its importance, thinks it’s a lot more insightful than it is and can’t think much beyond next week. Andy Burnham is right, the government shouldn’t be in hock to them. Burnham does need a coherent plan and narrative for government. But if that plan involves higher borrowing, slightly higher interest rates won’t be the end of the world. And if less austerity ultimately prevents Farage becoming PM, then the gilt market really would have dodged a bullet.

Finally, some contrarian commentary on the UK! Welcome to Substack Neville.